Optionality, leverage, and the price of waiting

Jin’s Notes: The Asking Price (Tool Kit)

I didn’t grow up hearing dinner-table conversations about marginal tax rates or mortgage stress tests. Like most people I know, I assumed “saving for a down payment” was the whole story. Good times.

I still believe that a home should be a sanctuary first. My goal is to buy a place that aligns with how I want to live at that moment in my life. Above all else, this is the priority.

But it will likely be the largest financial commitment I ever make. Protecting that sanctuary means understanding the tax structure and market mechanics around it. I’m not looking for a flip, I’m looking for something that’s both financially sound and personally grounding.

So here is the guide I wish someone handed me—fact-heavy, sourced, stitched together over a week of obsessive note-taking—so you don’t have to build an evidence board of your own. (Still grounded in the fact that I, too, am figuring this out in real time.)

In general, we’ll cover:

- How your taxes and first home purchase are intertwined

- Registered accounts (FHSA, RRSP, HBTC, and more)

- Tax deadlines you should know

- Mortgage rates

- Property taxes

- Land Transfer Tax (LTT)

- Principal Residence Exemption (PRE)

- My thought process

Your income isn’t your income

Canada operates under a progressive income tax system. According to the Canada Revenue Agency (CRA), federal tax rates increase as income rises, with provincial tax layered on top.

Picture pouring water into differently sized cups. The first fills at one rate. Once it’s full, the next portion spills into the next cup at a slightly higher rate. Only the overflow gets taxed more. That tax difference is called a marginal tax rate.

In Ontario, you pay both federal and provincial income tax, but file one return through the CRA. That means every dollar you earn passes through two filters before it becomes “yours.”

Why does this matter for housing?

Because your marginal tax rate determines how powerful certain saving strategies are. RRSP contributions, for example, reduce taxable income. If you’re earning enough to sit in a higher bracket, a tax deduction is worth more to you than it is to someone in a lower bracket.

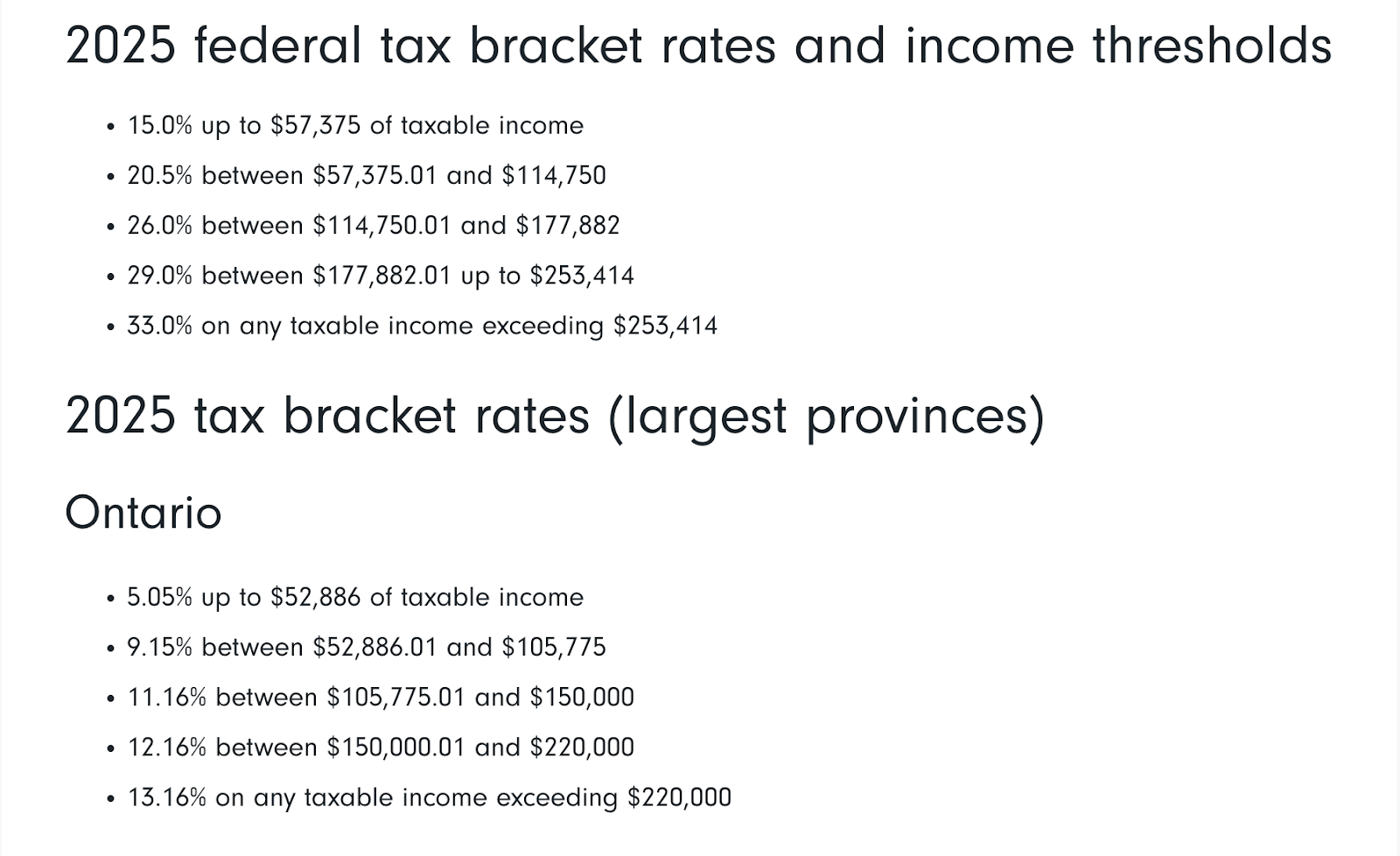

If you earn $75,000 in Ontario, portions of your income are taxed federally at 15 per cent, 20.5 per cent, plus Ontario’s provincial brackets. That rate translates how much tax relief you receive when contributing to a registered account. Below is a screenshot from Fidelity’s overview of 2025 Canadian income tax brackets.

So if someone makes $75,000, here’s what actually happens:

First $57,375 → taxed at 15 per cent

Remaining $17,625 ($75,000−$57,375) → taxed at 20.5 per cent

Your Notice of Assessment outlines your taxable income and contribution room. It’s issued annually by the CRA after your return is processed. If you don’t know what I’m talking about, thank goodness you’re here.1

Please leverage your Registered Accounts!!!

This is where tax policy stops being an abstract adult concept and starts directly affecting purchasing power.

1. A win-no loss situation: First Home Savings Account (FHSA)

According to the Government of Canada, eligible first-time homebuyers can contribute up to $8,000 per year to an FHSA, to a lifetime maximum of $40,000. Contributions are tax-deductible, and qualifying withdrawals to purchase a home are tax-free.

That combination, a deduction going in (like an RRSP) and no tax coming out (like a TFSA), is unusually generous. Not common within Canada’s tax code.

But, and this is the part people miss, you only start accumulating annual room after you open the account.

Plainly,

- Open an FHSA in 2026

- Contribute $0 that year

- In 2027, you can contribute:

- $8,000 (2027 room)

- plus $8,000 (unused 2026 room)

You could contribute up to $16,000 in 2027. But if you never open the account in 2026, you don’t accumulate that 2026 room.2

This is not an account you “should look into later.” It creates optionality, even without immediate contribution. Not opening it is like refusing free compounding because you’re “not ready.” The account doesn’t care about your timing anxiety.

Government programs are rarely altruistic, so I was skeptical too. To me, this one is seemingly designed to subsidize disciplined future homeowners. Use it.

(If you’re with TD, like me, here’s the link.)

Pair it with: the First-Time Home Buyers’ Tax Credit (HBTC)

These two distinct but correlated government programs are often used together, compounding homeownership affordability. 3

First Home Savings Account (FHSA), “savings tool”

- A registered account combining benefits of RRSPs (tax-deductible contributions) and TFSAs (tax-free withdrawals)

- No repayment, unlike the Home Buyers’ Plan (HBP)

- Benefit: Up to $8,000 per year ($40,000 lifetime) in contributions

- When to use: While saving, leading up to the purchase

First-Time Home Buyers’ Tax Credit (HBTC), “closing credit”

- A non-refundable tax credit (Line 31270) to help with closing costs

- No repayment, one-time credit

- Benefit: $10,000 × 15 per cent federal tax rate = $1,500 in tax relief

- When to use: In the year you purchase your home

The FHSA helps you save for a down payment with a $40,000 limit, the HBTC helps pay for closing costs with a flat $1,500 credit. Eligibility for one does not affect the other; they serve different purposes.

2. Borrowing from your future self: RRSP + Home Buyers’ Plan (HBP)

The Registered Retirement Savings Plan (RRSP) reduces your taxable income when you contribute. That’s its traditional role.

Under the Home Buyers’ Plan (HBP), the CRA allows eligible buyers to withdraw up to $60,000 from their RRSP to buy or build a qualifying home. If purchasing with a partner who also qualifies, that’s up to $120,000 combined.

Of course, this is not free money. You must repay the withdrawal to your RRSP over 15 years. If you miss a repayment in a given year, that portion is added back to your taxable income.

The HBP increases your short-term buying power (like a credit card). It can also reduce long-term retirement compounding if used carelessly (future you gets the bill).

*Zoom out for a second:

- HBP = interest-free loan from your RRSP

- You eventually pay tax on those funds in retirement

- FHSA funds, if used properly, may never be taxed at all

They’re close cousins and look similar. They’re not.*

3. The Workhorse: Tax-Free Savings Account (TFSA)

If the FHSA feels like a targeted government incentive and the RRSP feels like long-term retirement machinery, the Tax-Free Savings Account (TFSA) is a flexible middle child.

The CRA states that TFSA contributions are not tax-deductible. You contribute with after-tax dollars. However, investment growth inside the TFSA (earned interest, dividends, or capital gains) is not taxed, and withdrawals are tax free.

*Unlike an RRSP, withdrawals do not get added back to your taxable income.

RRSP: get the tax break upfront and pay later

TFSA: you pay the tax upfront and never again*

You can withdraw from a TFSA at any time, for any reason, without penalty (unlike the FHSA, which has a purpose restriction). Withdrawn amounts are added back to your contribution room the following calendar year.

For a future homebuyer:

- FHSA: = structured home fund

- RRSP via HBP = strategic leverage

- TFSA = liquidity

It can hold part of your down payment, cover some closing costs, or act as an emergency fund so you’re not house-rich and cash-poor on day one. Has anyone experienced moving into a new apartment and having three pieces of furniture for a month? Kind of like that. Multiplied by a couple hundred thousand.

Tax season deadlines you should know

The CRA has a pop-up of due dates and payment dates on their website. Here’s a few:

- March 2, 2026: Deadline to contribute to an RRSP, a PRPP, or an SPP

- March 2, 2026: T4 and T5 slips for most employers and payers

- April 30, 2026: Deadline to file your taxes

- June 15, 2026: Deadline to file your taxes if you or your spouse or common-law partner are self-employed

- If you owe money, interest begins accruing after these dates

- Dec. 31, 2026: Deadline to contribute to FHSA (to be deductible for that tax year)

- If FHSA taxes ever become payable on your account (for example, if you don’t buy a qualifying home), an FHSA tax return (RC728) and payment are due by June 30 of the year after the tax arises

If using HBP, withdrawals must occur in the year of purchase or in January of the following year.

The cost that dwarfs most credits: Mortgage Rates

Tax credits make headlines all the time.456 Mortgage rates do too (especially last week), although they’re probably more famously known for determining how well you sleep at night.

The Canada Mortgage and Housing Corporation (CMHC) has clear explanations on mortgages in their FAQ. For your convenience; a mortgage is simply a loan secured against your home. You borrow from a lender, agree to repay it with interest, and if you don’t, the lender has a legal claim to the property.

There are two timelines that matter:

Amortization = the total time it would take to pay off the loan, commonly 25 years in Canada

Term = the length of your contract with a lender, commonly five years

That means you renegotiate your rate multiple times before the mortgage is fully paid off. This is a terrible analogy and the only one I can think of:

Let’s say, because you’re insane, you sign up for a 25-year gym membership instead of paying an upfront cost of a million dollars to use their facilities (they’re also insane). The membership renegotiates every five years depending on how the economy feels about working out.

The Bank of Canada sets the policy interest rate, influencing borrowing costs nationwide. Commercial banks (RBC Royal Bank, for example) publish current fixed and variable mortgage rates, which you’ll typically choose between when the time comes.

Fixed rate: Your interest rate stays the same for your term; less volatility, potentially higher upfront cost

Variable rate: Your rate fluctuates with changes to the Bank of Canada’s benchmark rate; lower initial rate (sometimes), more sensitivity to economic shifts

Both carry trade-offs. What you decide will be based on your current situation.

Regardless of the exact rate on a given day, the structural lesson is as follows: a one-percentage-point change in mortgage rates can increase or decrease your monthly payment by hundreds of dollars.

And then there’s the mortgage stress test.

Under federal rules administered by the Office of the Superintendent of Financial Institutions (OSFI), borrowers must qualify at the greater of 5.25 per cent of their contract rate plus two percentage points. In other words, even if a lender offers you 5.5 per cent, you must prove you can afford roughly 7.5 per cent.

This is designed to protect borrowers and the financial system. It also reduces how much you can qualify for. The bank doesn’t care what you can afford today if you can’t afford it tomorrow.

Now layer that onto Toronto prices. That one-percentage-point change I just mentioned? Those hundreds of dollars on a typical GTA mortgage, over 25 years, compounds into tens of thousands.

Registered accounts determine how you accumulate the down payment, mortgage rates determine whether you can sustainably carry the asset once you have it.

The very real costs of your not-so-real home: Property Tax

Are we surprised there’s more to homeownership responsibilities than paying a mortgage? I hope not.

Property taxes function (sort of) like a subscription fee for living in your city. It funds transit, garbage collection, fire services, things like that.

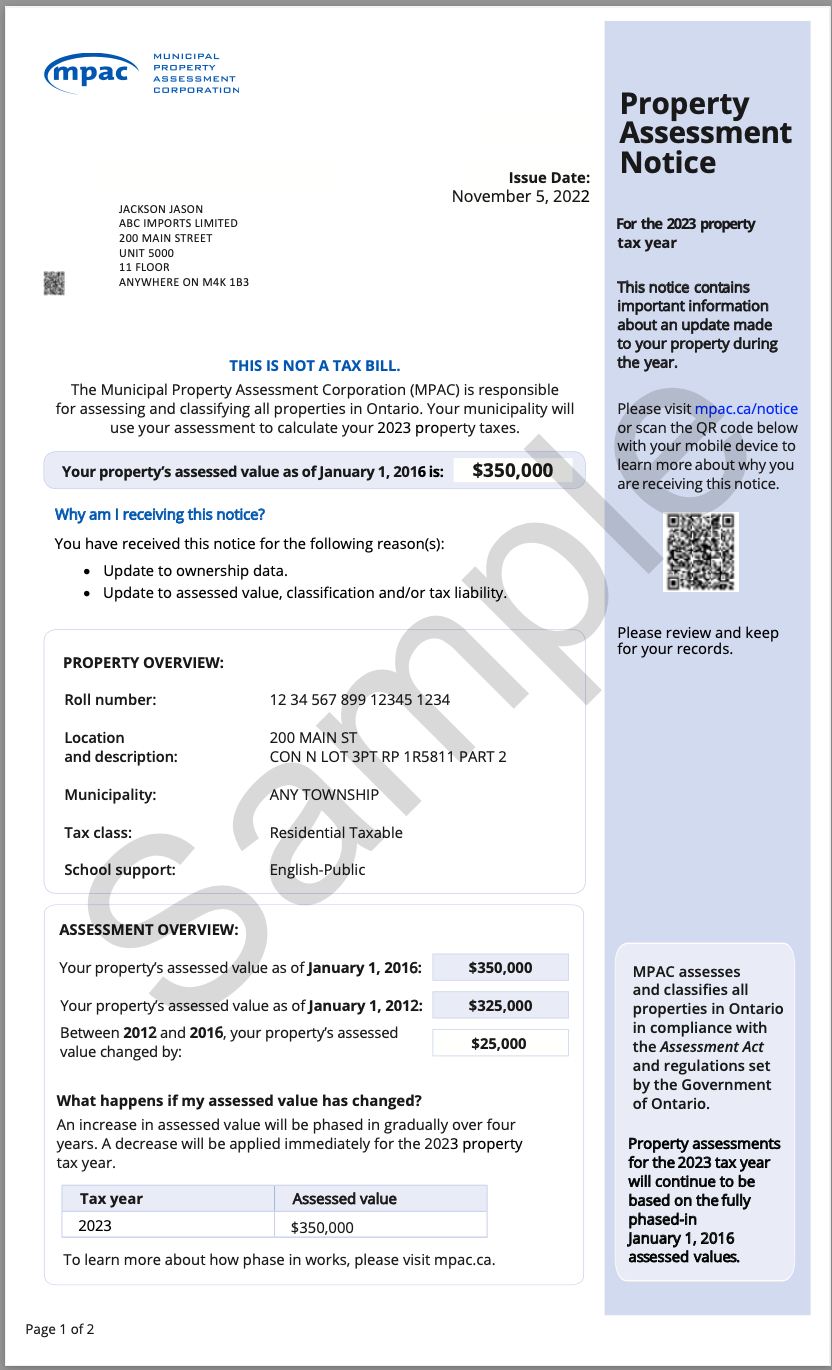

In Toronto, rates are set annually by the city. The value your tax bill is based on comes from assessments conducted by the Municipal Property Assessment Corporation (MPAC).7

If unpaid, interest accrues. In extreme cases, properties can be sold through tax sale.

To address the elephant in the room, yes. The property taxes also rise. Sometimes significantly.

Some more upfront shock, if this wasn’t enough: Land Transfer Tax

In Ontario, buyers pay a provincial land transfer tax (PLTT). In Toronto, buyers pay an additional municipal land transfer tax (MLTT). This effectively doubles the amount Torontonians owe, versus those anywhere else in Ontario. A second cover charge for those of us trying to enter the housing market.

The structures mirror each other (up to $400,000):

- $0–$55,000: 0.5 per cent

- $55,000.01–$250,000: 1.0 per cent

- $250,000.01–$400,000: 1.5 per cent

- Above $400,000, both Ontario (provincial) and Toronto (municipal) land transfer tax rates increase on a tiered scale, with higher brackets triggering progressively higher percentages.

Wait! Both the Province of Ontario and the City of Toronto offer significant rebates for eligible first-time homebuyers.

- Provincial Rebate (PLTT): Credit of $4,000

- Municipal Rebate (MLTT): Credit of $4,475

According to provincial and municipal guidelines, combined rebates for eligible first-time buyers can significantly reduce upfront tax burden, but only if you qualify and apply correctly. Many first-time buyers budget for the down payment and forget this entirely. That is a very expensive mistake.

Scenario

- Buyer: 30-year-old single professional earning an average Toronto salary of approximately $75,400

- Property: “Starter” one-bedroom condo in Toronto purchased for $550,000

- Affordability: Using a Mortgage Affordability Calculator, a single earner at this salary level typically qualifies for a home in the $320,000 to $550,000 range, depending on their down payment and debt levels

- PLTT: $7,475 (tax) – $4,000 (rebate) = $3,475

- MLTT: $7,475 (tax) – $4,475 (rebate) = $3,000

The buyer must pay a total of $6,475 ($3,475 + $3,000) at the time of closing. Without these rebates, the total tax bill would have been $14,950.

The “Golden Rule” of the Canadian tax system: Principal Residence Exemption (PRE)

From what I understand so far, the Principal Residence Exemption (PRE) is arguably one of the most powerful structural advantages in Canadian housing policy.

As stated by the CRA, when you sell a property designated as your principal residence, capital gains are generally exempt from tax. Unlike a typical tax credit, which reduces what you owe, the PRE eliminates the tax on that gain entirely, provided the property was designated as a principal residence for every year you own it.

Sell a rental property and 50 per cent of the capital gain is taxable. Flip homes frequently and profits may be treated as business income, which is fully taxable.

If you sell stocks and make money, the CRA wants a share. If you sell your primary home and make money, it usually doesn’t. Same profit, different rules.

That distinction in tax-advantaged assets can shape behaviour (to incentivize ownership.)

Your first home will hold so much personal value—years of your life will be nurtured by those four walls. But as much as housing is shelter, it is a tax-advantaged asset, under specific conditions. Understanding those conditions will change how you think about ownership versus investment.

Here’s what I’ve learned in trying to piece this together:

- Progressive income tax determines saving capacity

- Registered accounts alter taxable income and growth

- Mortgage rates determine sustainability

- Property taxes determine carrying costs

- Land transfer tax affects liquidity

- Capital gains rules shape long-term wealth

None of these operate in isolation.

Do you remember being given simplified rules in math class like “You can’t subtract a bigger number from a smaller one,” just to have it disproved the next year?

My friends and I used to complain about how half of the work seemed to be “unlearning” everything we thought we knew. Elementary arithmetics that fall apart in algebra and calculus. Housing finance seems similar (so far).

This post is just foundational knowledge. The kind that makes later nuance easier to understand. Once we grasp how the system is structured, we can engage with market shifts, policy changes, and personal trade-offs with more clarity.

I realized after an interview I did for the next post, that if I treat “saving for a down payment” as the sole hurdle, I’m missing the architecture that tries to support the entire system.

It won’t make Toronto affordable overnight. I’m not God. What it will do, though, is make you more fluent in the language of the decision. In a city where margins are thin, that difference matters.

Sources

General information

- https://www.canada.ca/en/revenue-agency/services/tax/individuals/frequently-asked-questions-individuals/canadian-income-tax-rates-individuals-current-previous-years/learn-progressive-tax-rates-income-brackets.html

- https://www.canada.ca/en/revenue-agency/services/tax/individuals/frequently-asked-questions-individuals/canadian-income-tax-rates-individuals-current-previous-years.html

- https://turbotax.intuit.ca/tips/what-is-the-marginal-tax-rate-and-how-does-it-work-in-canada-16253?srsltid=AfmBOop4g4opIgOrIaOPNx6pQ6haqfDx5XNx2ERDUJvEIxIvoFzbRVM2

- https://www.fidelity.ca/en/insights/articles/2025-canadian-income-tax-brackets/

- https://www.canada.ca/en/revenue-agency/news/cra-multimedia-library/individuals-video-gallery/webinar-individuals-modest-income/learn-about-your-taxes-about-notice-assessment.html

- https://www.canada.ca/en/services/taxes/income-tax/personal-income-tax/after-you-file/noa-nor.html

Registered Accounts

- FHSA https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/first-home-savings-account.html

- “Contibution Room” definition: https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/tax-free-savings-account/contributing/before.html#toc1

- Scenarios: https://www.canadianmoneysaver.ca/articles/3730

- FHSA account setup (TD): https://www.td.com/ca/en/investing/direct-investing/accounts/review?acc=FHSA

- HBTC https://www.canada.ca/en/revenue-agency/news/newsroom/tax-tips/tax-tips-2023/first-time-home-buyer-tax-incentives.html

- RRSP/HBP: https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/rrsps-related-plans/registered-retirement-savings-plan-rrsp.html

- https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/rrsps-related-plans/what-home-buyers-plan.html

- https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/rrsps-related-plans/what-home-buyers-plan/definitions-home-buyer-s-plan.html#qualifyinghome

- https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/rrsps-related-plans/what-home-buyers-plan/repay-funds-withdrawn-rrsp-s-under-home-buyers-plan.html#wb-cont

- TFSA https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/corporations/eligible-dividends.html

- https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/about-your-tax-return/tax-return/completing-a-tax-return/personal-income/line-12700-capital-gains/definitions-capital-gains.html

- https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/tax-free-savings-account/what.html

- https://www.canada.ca/en/revenue-agency/services/tax/international-non-residents/individuals-leaving-entering-canada-non-residents/newcomers-canada-immigrants.html

- https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/about-your-tax-return/interest-penalties/late-filing-penalty.html

- https://www.canada.ca/en/revenue-agency/services/tax/businesses/topics/completing-slips-summaries/financial-slips-summaries/rrsp-contribution-receipt-return/contribution-year.html

- https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/rrsps-related-plans/what-home-buyers-plan/participate-home-buyers-plan.html

Mortgage Rates

- https://www.canada.ca/en/financial-consumer-agency/services/mortgages/mortgage-terms-amortization.html

- https://www.cmhc-schl.gc.ca/consumers/home-buying/mortgage-loan-insurance-for-consumers/faqs-mortgage-loan-insurance?ap=a1-p1

- https://www.osfi-bsif.gc.ca/en/supervision/financial-institutions/banks/minimum-qualifying-rate-uninsured-mortgages#

- Stress test: https://trreb.ca/wp-content/files/homeownership/Mortgage-Stress-Test.pdf

- https://abcnews.com/US/wireStory/governors-tackle-rising-cost-living-relief-checks-tax-130005123

- https://www.cbc.ca/news/politics/carney-dropping-ev-mandate-introducing-new-emissions-standards-9.7075302

- https://globalnews.ca/news/11597160/gst-federal-rebate-credits-2026

- https://www.bankofcanada.ca/2025/06/understanding-policy-interest-rate

- https://www.bankofcanada.ca/core-functions/monetary-policy/key-interest-rate

- https://www.rbcroyalbank.com/mortgages/mortgage-rates.html

- https://www.ratehub.ca/variable-or-fixed-mortgage

Property taxes

- https://www.toronto.ca/services-payments/property-taxes-utilities/property-tax/late-tax-bill-payments

- https://www.toronto.ca/services-payments/property-taxes-utilities/property-tax/property-tax-rates-and-fees

- https://youtu.be/nrWry5i3TBU

- https://www.toronto.ca/home/311-toronto-at-your-service/find-service-information/article/?kb=kA06g000001cwNpCAI

- https://www.toronto.ca/news/city-of-toronto-launches-2026-budget

Articles

- https://www.cbc.ca/news/canada/toronto/council-debate-budget-2026-9.7081563

- https://globalnews.ca/news/11597160/gst-federal-rebate-credits-2026

- https://www.cp24.com/local/toronto/2026/01/07/heres-why-toronto-could-see-a-smaller-property-tax-increase-this-year

- https://www.cbc.ca/news/canada/toronto/toronto-budget-debate-tax-hike-1.7114394

Land Transfer Tax

- PLTT https://www.ontario.ca/document/land-transfer-tax/calculating-land-transfer-tax

- MLTThttps://www.toronto.ca/services-payments/property-taxes-utilities/municipal-land-transfer-tax-mltt/municipal-land-transfer-tax-mltt-rates-and-fees/

Rebates

- https://www.ratehub.ca/land-transfer-tax-ontario#

- https://www.toronto.ca/services-payments/property-taxes-utilities/municipal-land-transfer-tax-mltt/municipal-land-transfer-tax-mltt-rebate-opportunities

- Application https://www.ontario.ca/document/land-transfer-tax/land-transfer-tax-refunds-first-time-homebuyers

PRE

- https://www.canada.ca/en/revenue-agency/services/tax/individuals/topics/about-your-tax-return/tax-return/completing-a-tax-return/personal-income/line-12700-capital-gains/principal-residence-other-real-estate.html

- https://www.wealthsimple.com/en-ca/learn/capital-gains-tax-canada

- https://www.canada.ca/en/revenue-agency/news/newsroom/tax-tips/tax-tips-2018/flipping-houses-condos-know-your-tax-obligations.html